What Valet Parking has taught me about thinking terms of probabilities.

When it comes to Valet Parking, every establishment is different. From the high class restaurants to the hotels to the night clubs. Since I started, working the night clubs was always my favorite. It was always high volume in a short time frame. The places I worked, we would usually park anywhere from 100 to 200 cars in the span of about 6 hours, 9pm to about 3am. For the most part, night clubs are about status. Everyone going to these night clubs want to feel like they are important and getting the VIP treatment. In reality, they aren't. The only ones that really get the treatment, are the close friends of the club owners and the people that spend a considerably large amount of money.

Valet at a night club really isn't about convenience, at all. Why? Because everyone usually arrives at the same time and leaves at the same time. All the club goers want to be seen dropping their car off right in front of the club as well as it being returned to them right in front. So it would never make a difference how many valet attendants are working, at the end of the night, bar close, when everyone leaves at once, there is going to be a wait for your car. Tips are pooled, and since it really didn't matter how many valets were working, it made sense to under staff to make more cash. The less valets working, the less people that tips had to be divided up.

There is a high demand for rock staring, VIP-ing, or just plain leaving the car right in front where everyone can see it...what ever you want to call it. Back in the good old days we would have anywhere from 5 to 10 spots up front. Right there a function of supply and demand. The lower amount of VIP spots, the more it would cost to leave your car up front.

Why do people want their cars parked up front? They don't trust the valets parking their cars in the regular lot, they want to impress the women, the car is expensive, they don't want to have to wait for their car at the end of the night, status, they have drugs, guns or cash in the car, the list could go on...Either way, a waste of money.

What if they would have said no? I would have thrown the cars in the regular lot. Twenty minutes later another opportunity would present itself as a dealer would pull up and ask the same thing. All that mattered was how much money you would throw to have your car left up front. It didn't really matter to me who you were.

Rashad McCants, was one that I told plenty of times to get fucked. He never wanted to pay. I'm not going to leave your car up front just because you play for a horse shit basketball team.

How does this compare to trading? Edge and probabilities. If you haven't clearly defined your edge you are probably trading with out a trading plan. Trading is all about probabilities. You never know what trade will work out and which will not. Since that is the case, when your edge is present, you have to take the trade. Trying to pick and choose which you "think" will work will cause you to pass on many winning trades.

I knew back then, when valet parking what my edge was as well as I can clearly define my edge trading. Can you?

Valet at a night club really isn't about convenience, at all. Why? Because everyone usually arrives at the same time and leaves at the same time. All the club goers want to be seen dropping their car off right in front of the club as well as it being returned to them right in front. So it would never make a difference how many valet attendants are working, at the end of the night, bar close, when everyone leaves at once, there is going to be a wait for your car. Tips are pooled, and since it really didn't matter how many valets were working, it made sense to under staff to make more cash. The less valets working, the less people that tips had to be divided up.

There is a high demand for rock staring, VIP-ing, or just plain leaving the car right in front where everyone can see it...what ever you want to call it. Back in the good old days we would have anywhere from 5 to 10 spots up front. Right there a function of supply and demand. The lower amount of VIP spots, the more it would cost to leave your car up front.

Why do people want their cars parked up front? They don't trust the valets parking their cars in the regular lot, they want to impress the women, the car is expensive, they don't want to have to wait for their car at the end of the night, status, they have drugs, guns or cash in the car, the list could go on...Either way, a waste of money.

The best clubs to work were the hip hop clubs. Where the bangers, pimps, dealers, jersey chasers, and athletes would frequently hang out. Why? Because, apart from the athletes, their cars were everything to them. The going rate to leave your car up front would be 50 bucks. As soon, as someone pulled up in either a donk or expensive car, with out doubt they would ask, "How much to leave it up front?" Typically, if you knew they were a drug dealer or athlete they would pay the most to have their cars left up front. There is my edge. After working a spot for an extended period of time, you get to know people, who they are, what they do, and where they are from.

I remember a night when Fred Smoot, Dwight Smith, and Pat Williams came in. All three of them in their white Rolls Royce Phantoms. Of course they wanted them up front. All I said, was I had one spot left that was going to be a hundred bucks, I could open up two other spots for the same price. As I would have to take down someone that had thrown eighty bucks. Not a problem and easy as that. My edge was, Athlete, Five Hundred Thousand Dollar car, and I knew how bad they wanted them up front. My edge was there so I pressed it. At the time, I had maybe one or two cars up front. Plenty of space.What if they would have said no? I would have thrown the cars in the regular lot. Twenty minutes later another opportunity would present itself as a dealer would pull up and ask the same thing. All that mattered was how much money you would throw to have your car left up front. It didn't really matter to me who you were.

Rashad McCants, was one that I told plenty of times to get fucked. He never wanted to pay. I'm not going to leave your car up front just because you play for a horse shit basketball team.

How does this compare to trading? Edge and probabilities. If you haven't clearly defined your edge you are probably trading with out a trading plan. Trading is all about probabilities. You never know what trade will work out and which will not. Since that is the case, when your edge is present, you have to take the trade. Trying to pick and choose which you "think" will work will cause you to pass on many winning trades.

I knew back then, when valet parking what my edge was as well as I can clearly define my edge trading. Can you?

Conversation with a maverick investor Investment legend William O’Neil shares his market wisdom

By Kevin Marder

LOS ANGELES (MarketWatch) — The peanut-butter/chocolate moment in this trader’s career occurred in 1990. Midway through reading a book on how to make money in stocks, a giant light bulb switched on.

Suddenly it was as if the mysteries of the market — how to find big-winning stocks, why the market did what it did when it did, how to interpret the market’s message, when to become defensive and move to a cash position, among them — were no longer mysteries.

At that moment, the fog had cleared and all the elusive pieces in the puzzle came together.

This trader was so excited that he put the book down and began pacing the living room floor, pondering all the possibilities. It all made sense now. At last.

The book, “How To Make Money In Stocks” by William J. O’Neil, went on to become a runaway best-seller. The strategy, known by the acronym “CAN SLIM,“ was based upon an exhaustive research study conducted by O’Neil in the early-‘Sixties. In it, O’Neil looked at all of the biggest-winning stocks of the prior decade to see if they shared common characteristics. In fact, they did. O’Neil discovered there were seven key traits in each big winner, and he assigned each a letter, which comprised the trademark term CAN SLIM.

O’Neil, a young stockbroker at the time, proceeded to take this valuable information and began applying it to his account and those of his clients. Starting with $4,000 or $5,000 plus some borrowed money and use of margin, O’Neil had three big, back-to-back winners in his account beginning in late 1962. By the fall of 1963, the profits exceeded $200,000 and O’Neil proceeded to buy a seat on the New York Stock Exchange.

O’Neil went on to found a successful institutional research business and, in 1984, a newspaper, Investor’s Business Daily , for which he continues to serve as chairman.

It is difficult to think of anyone having influenced more of this era’s most outstanding investors than O’Neil. Plenty of individual investors using CAN SLIM have clocked triple-digit annual gains in their accounts. Given the influence of the man on this trader and this column, it made sense to include the following interview, the first of two parts, and conducted via e-mail.

Q: Bill, in your 50 years of experience in the market and working with investors, what is the biggest mistake the average investor makes?

A: Not having, and following, a strict rule to always sell and cut short your losses.

Q: What is the most important personality trait that an investor should have to become successful in the market?

A: Willingness to work hard and correct your major weak points.

Q: It has been said that a woman makes for a better investor than a man because a woman is less likely to let her ego get in the way of making investment decisions. Do you agree?

A: It all depends on if a person is motivated and determined to learn how to invest successfully and learn from their mistakes.

Q: Some people are convinced the game is rigged. What would you say to them?

A: I’ve never met a successful pessimist.

Q: Along these lines, in the past few decades, more investors appear to have thrown in the towel than any time in recent decades. Do you view this as a periodic cleaning-out process that needs to take place every so often or perhaps something more ominous?

A: No, it is the aftermath and severe unintended consequences of our government in 1995 and thereafter, mandating to banks and lenders whom they must make home loans to, or face penalties.

Q: For decades, trading volume had been dominated by institutional investors such as mutual funds, pension funds, insurance companies, bank trust departments, etc. Their accumulation of a stock would clearly show up on a price/volume chart, and the same thing with a chart of an index such as the Industrials. Over the past three years, high-frequency trading has come to comprise a purported 60% of all trading volume. Doesn’t this fact make the volume that we see on stock charts and index charts less reliable as a means of detecting accumulation or distribution?

A: Not necessarily. The focus of supply and demand doesn’t change, and price and volume are still the best tool to carefully analyze supply and demand.

Q: Other than a relative strength line and a moving average, do you ever use other technical indicators?

A: Very few. We use more fundamentals like accelerating earnings and sales growth, unique new products gaining market share, high ROE or pre-tax margins, good sponsorship, innovative entrepreneurial management, etc.

Q: Why is it that you prefer looking at weekly price/volume charts than daily?

A: That’s how I started learning to recognize sound patterns under accumulation, and am still more accurate with weekly charts. They also give me a better overall picture. However, I also check both daily and long-term monthly charts.

Q: I know in your first book you mention that only the price/volume behavior of the major averages and action of the leading stocks matters when it comes to general market analysis. We are not long-term investors, but to me the cumulative NYSE advance-decline line has value as a long-term indicator when it begins to diverge from the averages in a mature bull market. Do you have any use for the cumulative advance-decline line at all?

A: The A/D line is not a very precise timing tool and can sometimes be way too early. We’ve done very well in most cases by ignoring it.

Q: Many investors using your strategy seem to view the follow-through day concept as a sort of magical elixir. Debates take place over how a follow through day should be interpreted. What would you say to them?

A: Keep studying, and go to a few workshops, like IBD’s Chart School Seminar.

Q: You have been through so many market cycles. Over the years, have you seen any changes in the patterns that stocks make on their price charts?

A: The law of supply and demand and human nature remain the same. Chart patterns also remain the same. So the wise investor should learn to accurately read proper patterns.

Q: In your first book, you mention that a typical growth stock will break out of a base and run up 20%-25% before pausing and perhaps building a second base. Does this still take place in a typical market leader, or is the move less than that after breakout?

A: It can vary depending on the type of market or stock you’re in.

Q: You are a big proponent of owning stock in younger, entrepreneurial companies with innovative new products and services. Earlier this year, we began to see the IPO market perk up, at least until the recent market turbulence. What will it take to revive this engine of growth?

A: A new administration that believes in the free enterprise system, which led every market cycle for the past 150 years.

Q: I have always felt that because each human being has a unique makeup of temperament, risk tolerance, experience, etc., an investor should take a strategy such as yours, or any other strategy for that matter, and make it their own by personalizing it. How do you feel about this?

A: That’s OK, but frequently trying to add to our system or tweak it doesn’t make it better. It’s hard enough to learn all the realistic rules and have the discipline to always follow them. So, concentrating on getting it all down and executing is in my view, the road to real investment success. IBD has thousands of investors that learned how to become winners, but it took them time to make it work. It’s not easy. Persistence helps.

Q: Along these lines, what changes do you make in your own trading as compared with the guidelines of the CANSLIM methodology?

A: Very few.

Q: The Fed has its hands tied and fiscal stimulus is a bad word in Washington due to the large federal budget deficit. With this in mind, what concrete steps should the administration and Congress take to jump-start growth?

A: Democrats control the Presidency and the Senate. They control government policy which has not worked well. It will probably require new management to take place months after the November election to create strong tax incentives to start small businesses and help existing ones. Our studies show small business creates 80% of our job ... not the 60% our government incorrectly believes. Increasing taxes and spending more money is not a sound answer. It just creates more problems.

Q: The bond market is certainly prepping for either a recession or a zero growth economy. Do you expect the U.S. to follow the way of Japan and enter a deflationary era?

A: I don’t predict.

Fitting in his location far from the canyons of Wall Street in Los Angeles, O’Neil does not concern himself with personal opinion or prediction. All that matters is fact and historical precedent. Of course, this is the diametric opposite of most other market seers.

His landmark research study of the early ‘60s was built on pure common sense and logic: Look at the biggest market winners of the past and see if a common thread runs among them. Then look for these seven characteristics in stocks of the future, and employ sound money management rules to protect precious capital when you either make a mistake or the general market flounders.

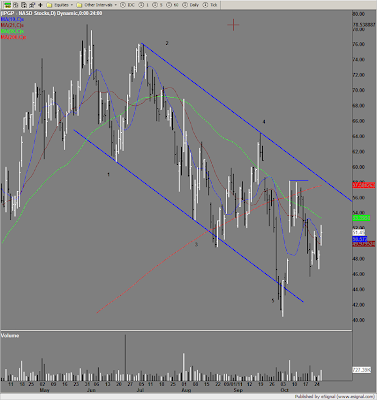

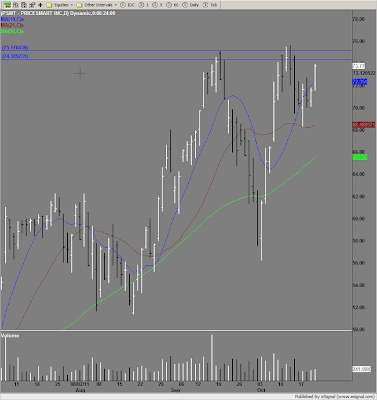

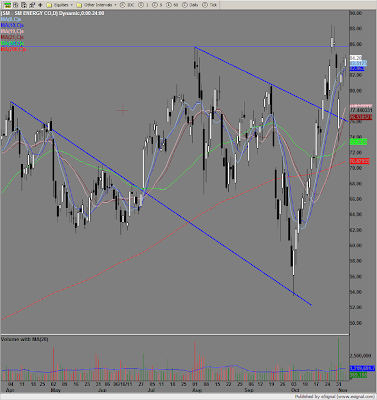

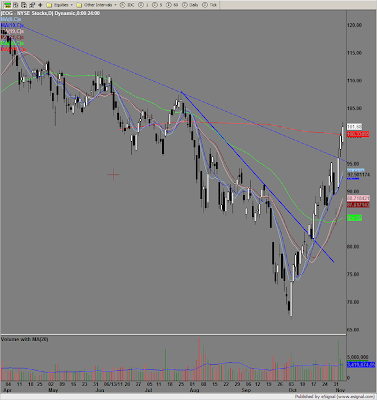

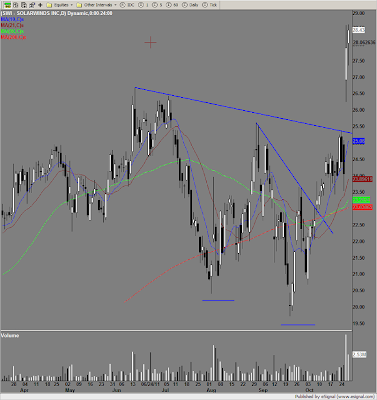

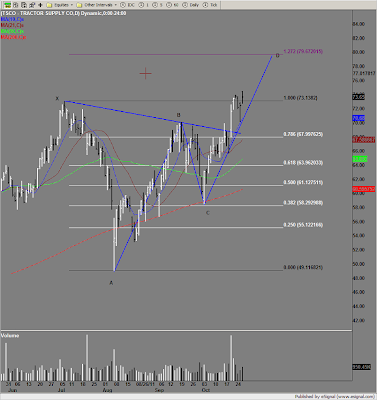

IPGP Follow up

Trade hasn't triggered. No point in getting chopped up with in the channel.